The US equity and bond markets have been anticipating central bank rate hikes for some months now, and this anticipation is almost entirely responsible for the sharp sell-off that has been taking place across the board but especially in the stocks of smaller and more "future-oriented" companies.

We have already written about how we find the conventional wisdom to be nonsensical on this point: see "Conventional Wisdom misses the mark (as usual)."

Today (26 January), after the first Federal Reserve Open Market Committee meeting of 2022, the Fed issued this statement and then Fed Chairman Jerome Powell held a press conference, which you can watch here.

During the press conference, equity markets plunged at remarks that the Fed has "plenty of room to raise interest rates without threatening the labor market" (see statements beginning at the 0:42:00 mark of the video).

Mr. Powell then went on to say that, in contrast to previous conditions: "the economy's much stronger and inflation's much higher, and I think that leads you to -- and I've said this -- being willing to move sooner than we did the last time, and also perhaps faster" (at 0:45:25 and following).

The markets don't want to hear about "sooner" or "faster" or "plenty of room," but we are already on record as saying that the Fed should just get it over with and raise rates, and get out of what are basically the "emergency low rates" that have been in place, with little variation, since 2020 -- and indeed since 2008 and 2009!

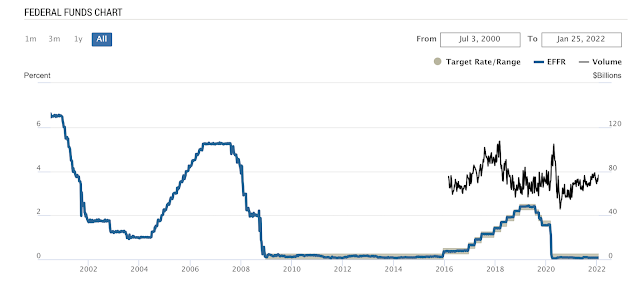

Fed Funds Rate since July 2000 -- left Y-axis has the rate in percentage points.

Source: NY Federal Reserve (link).

Our opinion is that the Fed needs to put aside the "kid gloves" and stop babying the markets, and just raise rates -- preferably faster rather than dragging it out. They should just raise rates by 50 basis points (half a percent) at each of the next two meetings (for a total of 1%) and then stop to see how that goes.

We are not worried about the markets dropping in anticipation of Fed rate hikes -- and we don't believe that the Fed should be worried about it either.

Market corrections are necessary! While they are never pleasant for investors, market corrections represent a "shakeout" of some of the over-speculative behavior that inevitably accompanies any positive market action. These shakeouts need to happen.

The bigger problem in the economy right now is seen in the supply chain issues -- these are real challenges, and they cannot be fixed with overly-accommodative monetary policy. They stem from a variety of factors, including an ongoing shift towards holding smaller inventories and relying on "just-in-time" logistics, with little margin for error. This left supply chains ripe for disruption during the events of 2020 and the policies enacted by governments around the world in response. And they will take some time to get fixed -- but the Fed has no role in fixing them.

In fact, increasing the money supply at a time when the real supply of goods and services is constrained is a recipe for inflation, and as everyone can plainly see (and as the Fed indicated in the published remarks), inflation is impacting everyone right now.

Which is why we believe it is time for the Fed to take off the kid gloves and stop worrying about market hissy fits.

And for investors, we continue to advise ownership in well-run businesses positioned in front of fertile fields for future growth -- and continuing to own those companies through the many cycles and shakeouts that inevitably arise, including the one we are going through at the moment.

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.