Switching horses in midstream gets you on a performance treadmill.

Continue Reading

Episode 29: FTX-Human Nature At Work

Gerry closes the book on FTX...at least until more disturbing details come up.

Continue Reading

Episode 28 Leverage...It Always Works Until It Doesn't

The first of two episodes on the FTX fiasco.

Continue Reading

Episode 27: This Podcast Is Stuck In A "Trading Range"

It's 2 steps forward and 2 steps back for the market, leaving Gerry and Doug to try to make sense of it all. Actually, Gerry actually tries to make sense of it while Doug just snipes in with questions and comments.

Continue Reading

Episode 26: Free Enterprise Vs. Free Markets

Gerry and Doug talk books and then Gerry tells Doug why "free enterprise" isn't the same as "free markets".

Continue Reading

Episode 25: Who Do You Truss?

England's quits pro-growth and then the PM quits England.

Continue Reading

Episode 24: Just Like Kidney Stones, Bad Markets Eventually Pass

The current regime is stunting growth. This doesn't mean we need to panic.

Continue Reading

Episode 23: Fiat Finance, Families and Fake Fascists

Gerry and Doug go around the horn on a variety of issues, some of which don't even start with the letter "F".

Continue Reading

Episode 22: Putting Q3 Out of Our Misery

Gerry bids a not-so-fond goodbye to the quarter that was.

Continue Reading

Episode 21: Still Fed Up

The Fed continues to zig and zag, then over-zig and over-zag.

Continue Reading

Episode 20: Why Long Only?

Gerry and Doug think it's finally time to explain the show's name.

Continue Reading

Episode 19: Blue Skies Ahead

Gerry thinks the economy might be overcoming awful policy.

Continue Reading

Episode 18: ESG-A Bandwagon We Never Rode On

This week, Gerry laments the fact that he was anti-ESG before it was cool. Is Doug buying it? Listen to find out.

And find it on iTunes here so you can subscribe.

Continue Reading

Episode 17: What's Good

Gerry and Doug try to go against the grain and talk about positive developments in the investing world.

Continue Reading

Episode 16: The Heart of the Matter

Gerry and Doug riff on the economy and even work in some talk about the state of the music business at the end.

Continue Reading

Episode 15: And Then There Were Three

Dave Mathisen, the Director of Research at Taylor Frigon, joins Gerry and Doug to talk about his path to working in the financial world and hus role in the investing process.

Continue Reading

Episode 14: It's All About Suffering

Gerry talks about how suffering is part and parcel to successful investing.

Continue Reading

Episode 13: We Don't Do The Market

It might sound counterintuitive, but Taylor Frigon isn't interested in playing the normal stock market game.

Continue Reading

Episode 12 "Value" Investing Is Now Available

On this episode, Gerry discusses how his faith and worldview shape Taylor Frigon and how totally avoiding the issue is practically impossible in the current climate.

Gerry Frigon on "Money Life with Chuck Jaffe"

Gerry recently appeared on Money Life in the Market Call segment at the 33:00 mark to discuss growth investing and the market's slow start to the year. Please give it a listen!

Follow Chuck on Twitter at @ChuckJaffe and the show is at @MoneyLifeShow. Also, look for the show at @MoneyLifeShow on Facebook and on Instagram at @chuckjaffe.

Economic Growth as a Cure for Inflation

We have written about the wisdom of Art Laffer in numerous previous posts -- including some from the depths of the financial crisis of 2008 - 2009, such as this one: "What NOT to do about the market right now."

Recently, Art Laffer gave an interview with Michelle Makori on Kitco News (affiliated with Kitco Metals, of Montreal) in which he addressed some very important issues which are front and center in many of the discussions we are hearing from Wall Street and also conversations we are having with company management teams in the current economic situation.

Specifically, the subject discussed is inflation, which is of course extremely destructive to both businesses and households. Much of the angst on Wall Street over the past several months has to do with inflation, and with the concern that, in order to curb inflation, the Fed needs to increase interest rates -- even if it means causing a recession.

In fact, some commentators have explicitly argued that higher rates of unemployment are the only thing that will bring down inflation. Most notably, Larry Summers -- former US Treasury Secretary (from 1999 - 2001), former director of the National Economic Council (from 2009 - 2011), former Chief Economist of the World Bank Group (from 1991 - 1993), former President of Harvard University (from 2001 - 2006), and current professor at Harvard -- has been on record since June saying that the US economy needs to see multiple years of unemployment above 5.5% or 6%, or at least one year of unemployment as high as 10%, in order to curb inflation.

For examples of Larry Summers making these proclamations, see for example here, here, and most-recently here.

While his position may represent an extreme example, it crystalizes much of the conventional wisdom dominating the inflation discussion in recent months -- the idea that in order to tame inflation, the country just needs to "take its medicine," even if that leads to recession and dramatic increases in unemployment.

That's why this new interview with Art Laffer is so important -- because it directly refutes that prescription, and argues that the best way to deal with inflation is through pro-growth policies that enable the economy to produce more goods and services (and which, by the way, will actually lead to more employment).

Here are a few key quotations from Art Laffer in the above interview:

Beginning at about 08:45 in the video

"No -- you don't need a recession to bring down inflation. That's a Larry Summers model. We don't need a recession. In fact, when we got rid of inflation with Reagan, we had one of the biggest booms ever. In the 1920s they did the tax cuts: a huge boom, and prices actually fell during that period. John F. Kennedy, with the huge tax cuts in the 1960s -- a huge boom: the go-go 60's it was called. Inflation was down and we had a surplus in the budget. That's what we really need is pro-growth fiscal policy, and also other regulatory policy, and we need tight money policy by letting interest rates be higher than the rate of inflation. That's what we need and that would solve it, very quickly, without a recession."

At this point, interviewer Michelle Makori asks Art Laffer to specifically address the arguments of Larry Summers, paraphrasing that argument as: "It's very unlikely that we're going to see inflation come down to target range without a significant economic downturn [. . .], a significant interval and 6% unemployment."

Art Laffer responds:

"If the demand for a product drops, what happens to the price? It goes down. Now, if the supply of the product increases, what happens to the price? It goes down. Which way would you prefer to have it? A crash in the economy to get the price down, which is what Larry Summers says? Or my way: increasing the supply of goods and services so we have a boom, that brings down inflation, which is what we did with Reagan, Kennedy, and the 1920s?"

We strongly encourage everyone to watch this recent interview in its entirety, and consider these points whenever someone argues that we need a recession or high unemployment (both of which are catatrophic for individuals, families, and the economy in general) in order to reduce inflation.

There is a better way: economic growth!

As Art Laffer says in the above interview: "You grow out of price increases. If you have higher prices -- you produce more goods!"

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

The Latest Episode of The Long Only Podcast

Please listen, subscribe, review and share. Is is available on iTunes, as well as a separate page on the website. We generally release new episodes weekly.

Introducing: The Long-Only Podcast!

We have a separate page on the website for it, but we wanted to share the episodes of our new project, The Long-Only Podcast here. Please listen, subscribe, review and share. We hope to use these as a valuable tool in sharing our opinions and insights going forward. We generally release new episodes every Monday.

Continue Reading

Don't get off the train, May 2022 edition

image: Wikimedia Commons (link).

The vicious equity selling we have been witnessing in the markets is uglier than anything we've seen since the days of the dot-com crash of 2000 to 2002.

Different from the dot-com crash, however, is the fact that the selling is targeting some of the best growth companies for the most aggressive selling: these are legitimate companies with real business models and in many cases very strong earnings, and yet the price action we are seeing is as if the markets are looking for the strongest names and selling them mercilessly.

Professional traders with whom we work have noted that the selling appears to be driven by algorithms -- they are not seeing humans behind these trades. Instead, they see the market action as being primarily driven by automated non-human trading activity -- with perhaps as much as two-thirds of all trades being driven by high-frequency algorithms which are programmed to pursue the "meme of the day."

At present, the "meme of the day" involves variations on the theme of "inflation is bad for growth companies" and those are the companies that are being sold most aggressively. We have written about our reasons for disagreeing with this conventional wisdom -- see for example this previous post from January of this year.

But sell-offs like the one we are witnessing now definitely create the kinds of times that really "test your mettle" and your convictions as an investor.

Our convictions are very clear and based on our own thirty-six years of professional investing experience, as well as the professional investing experience of our mentor Dick Taylor and of his own mentor Thomas Rowe Price, that owning shares in well-run innovative businesses is always the best way to weather the inevitable storms, and that shares in those companies almost invariably outperform on the way back up after those storms run their course.

While the storm is raging, however, we advise following our saying: "Be centered -- be still."

We have written about this philosophy many times in the past, including in this previous post from 2011, in which we explain that when we say "be centered," we mean to "remain within a consistent discipline, and not make rash departures from that discipline." We also explain in that post that when we say "still" we do not mean "taking no action" but rather "continuing to act within the principles of an investment process."

One other phrase which we also offer to investors in times like these is the saying "Don't get off the train." We have written about this concept many times in the past as well -- including in this post which we published on March 2nd, 2009 -- just a week before the bottom of the 2008-2009 bear market. One month later, we wrote a follow-up post entitled "Don't get off the train -- revisited" with some reflections on why this concept is so important and how the events of the following month proved its validity.

The upshot of this saying is that investors should not panic-sell shares of good companies in times like these -- and those who have the means to do so might even consider selectively buying at these levels.

It can be very difficult to stick to one's convictions during times when the world seems to have lost its mind. However, we are convinced that the rules of good business and indeed common sense have not been repealed -- and we look forward to the day when they return.

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

TD Ameritrade interviews CIO, Gerry Frigon, on AT&T, VZ & T-Mobile earnings

The competition is cut-throat, says Gerry Frigon. He talks about ingesting in 5G and telecom stocks. He discusses why he has moved away from investing in Verizon (V), AT&T (T), and T-Mobile (TMUS). He also goes over finding yield and dividend-paying stocks in today’s market. Tune in to find out more.

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

Investment Climate April 2022: Stay Positive!

It has been a rough ride for the stock prices of the fastest growing companies in the economy over the last several months. While the short-term market machinations are not something we try to predict, the wild swings of late have been considerable and, for many, unnerving. Interestingly, the businesses in our Income Strategy (or what we consider internally our “stable, but slower growth businesses”) have been doing well versus general market averages. Nonetheless, while we thoroughly understand the consternation that these environments can often engender, we have always said that what matters most for long-term investors is a focus on the actual businesses of the companies in which we are invested and not the daily market prices at which companies are traded. This is not to say the market prices are never a consideration, but they are far down the list compared to the analysis of the businesses themselves.

While the market values of most growing companies have dropped in recent months, albeit for reasons we believe are somewhat silly, when looking at the underlying businesses of our portfolio companies, we would be hard-pressed to explain why they are down in market value. We don’t know when this environment will turn back to focus on business fundamentals as opposed to what the Federal Reserve is going to do, or what Vladimir Putin has up his sleeve, but we do know that if they continue to do as well in their respective businesses as they are now, the market values will take care of themselves just fine! Here are a few examples:

Grid Dynamics Holdings, Inc. helps Fortune 1000 companies in “digital transformation,” which involves discussions with the client about strategy and then collaborative creation of innovative digital products and experiences and new digital platforms, delivered at enterprise scale. The company has a market capitalization of about $1 billion, with annual sales around $250 million, and has a high percentage of employees (around 45%) who were located in Ukraine. Despite the massive disruption caused by the ongoing war, Grid recently raised its revenue guidance for the most-recent quarter to $65 million-plus, up from a previous guided range of $55 to $60 million (and up from about $39 million for the same quarter a year before). This level of business growth in the midst of a conflict of this magnitude demonstrates the professionalism of the leadership that can be found in our companies. As a side note, Grid management hired buses to move Ukraine-based employees and their families to safer locations, where they rented a five-story office building where employees could house their families on three of the floors (with showers and access to kitchen facilities) and have a space to work on the other two floors of the same building.

InMode, Ltd. is a leading designer and manufacturer of medical devices used for minimally-invasive and invasive surgical procedures, primarily for aesthetics or cosmetic surgery, including procedures such as body contouring, skin resurfacing, and collagen contraction, among others. The company presently markets ten different platforms supporting a wide range of procedures, and is a leader in the aesthetic surgery space. InMode presently has a market capitalization of about $2.9 billion on annual revenues of around $400 million, and recently pre-announced first-quarter results with expected revenues of $85 million, ahead of the previously guided range of $80 to $83.9 million, which itself was well above the $65 million from the year-ago period. We believe that InMode will continue to benefit from the growth of demand for aesthetic procedures that can provide dramatic results but which are less invasive than full-scale plastic surgery (and which also have shorter recovery times than most plastic surgery).

Dutch Bros, Inc. only recently became public in September of 2021, and is a newer addition to our Core Growth Strategy. Dutch Bros operates a chain of drive-thru shops that serve high-quality beverages, including coffees, blended drinks, espressos, and energy drinks in a wide variety of flavors and creative combinations. The company is focused on providing a high-quality customer experience characterized by friendly customer service and unparalleled speed and efficiency of delivery, including innovations to help customers get their order faster and get on their way instead of staying stuck in line at the drive-thru. Dutch Bros is one of the fastest-growing drive-thru companies by store count, with 538 stores at the end of 2021 (up from 254 at the end of 2015), and operating in twelve western and southwestern U.S. states (up from seven at the end of 2015). The company believes that they can easily get to 4,000-plus stores in the U.S. over time, and external analysis by ourselves and others suggests that this number is probably conservative, and may be in the range of 6,000 potential stores, or even higher. Dutch Bros market capitalization is presently about $8.3 billion, on annual revenues of about $500 million in 2021 (likely to be above $700 million in 2022). We recommend visiting a Dutch Bros drive-thru in your area if possible: they typically have long lines throughout the day, but they are well-organized to get customers through the lines and on their way in a timely and positive fashion.

In tough markets, it is because we have conversations with companies like the above-mentioned that we stay so overwhelmingly positive on the long-term outlook.

Stay tuned for more commentary in between the quarterly Investment Climate publication either through our blog on our website (www.taylorfrigon.com), or through our new podcasts that will be coming out soon!

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

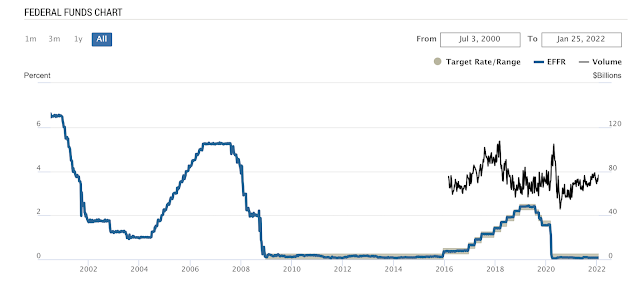

Just take off the kid gloves already!

image: Wikimedia Commons (link).

The US equity and bond markets have been anticipating central bank rate hikes for some months now, and this anticipation is almost entirely responsible for the sharp sell-off that has been taking place across the board but especially in the stocks of smaller and more "future-oriented" companies.

We have already written about how we find the conventional wisdom to be nonsensical on this point: see "Conventional Wisdom misses the mark (as usual)."

Today (26 January), after the first Federal Reserve Open Market Committee meeting of 2022, the Fed issued this statement and then Fed Chairman Jerome Powell held a press conference, which you can watch here.

During the press conference, equity markets plunged at remarks that the Fed has "plenty of room to raise interest rates without threatening the labor market" (see statements beginning at the 0:42:00 mark of the video).

Mr. Powell then went on to say that, in contrast to previous conditions: "the economy's much stronger and inflation's much higher, and I think that leads you to -- and I've said this -- being willing to move sooner than we did the last time, and also perhaps faster" (at 0:45:25 and following).

The markets don't want to hear about "sooner" or "faster" or "plenty of room," but we are already on record as saying that the Fed should just get it over with and raise rates, and get out of what are basically the "emergency low rates" that have been in place, with little variation, since 2020 -- and indeed since 2008 and 2009!

Fed Funds Rate since July 2000 -- left Y-axis has the rate in percentage points.

Source: NY Federal Reserve (link).

Our opinion is that the Fed needs to put aside the "kid gloves" and stop babying the markets, and just raise rates -- preferably faster rather than dragging it out. They should just raise rates by 50 basis points (half a percent) at each of the next two meetings (for a total of 1%) and then stop to see how that goes.

We are not worried about the markets dropping in anticipation of Fed rate hikes -- and we don't believe that the Fed should be worried about it either.

Market corrections are necessary! While they are never pleasant for investors, market corrections represent a "shakeout" of some of the over-speculative behavior that inevitably accompanies any positive market action. These shakeouts need to happen.

The bigger problem in the economy right now is seen in the supply chain issues -- these are real challenges, and they cannot be fixed with overly-accommodative monetary policy. They stem from a variety of factors, including an ongoing shift towards holding smaller inventories and relying on "just-in-time" logistics, with little margin for error. This left supply chains ripe for disruption during the events of 2020 and the policies enacted by governments around the world in response. And they will take some time to get fixed -- but the Fed has no role in fixing them.

In fact, increasing the money supply at a time when the real supply of goods and services is constrained is a recipe for inflation, and as everyone can plainly see (and as the Fed indicated in the published remarks), inflation is impacting everyone right now.

Which is why we believe it is time for the Fed to take off the kid gloves and stop worrying about market hissy fits.

And for investors, we continue to advise ownership in well-run businesses positioned in front of fertile fields for future growth -- and continuing to own those companies through the many cycles and shakeouts that inevitably arise, including the one we are going through at the moment.

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

Investment Climate January 2022

Image from https://www.hp.com/us-en/shop/tech-takes/top-7-augmented-reality-experiences

The equity markets, and particularly the stocks of growth companies, have been caught up in a major sell-off that started in November and which accelerated into the close of the year. It has continued in the early weeks of January as well. A recent article published in Bloomberg News notes that fully 40% of stocks on the NASDAQ composite are down 50% or more since their all-time highs -- a situation reminiscent of the dot-com crash in 2000. (https://www.bloomberg.com/news/articles/2022-01-06/number-of-nasdaq-stocks-down-50-or-more-is-almost-at-a-record)

The sell-off appears to be related to Fed rate-hike fears and interest-rate inflation noise. The Bloomberg article, for instance, declares: "Traders were quick to unload tech shares, whose high valuations become harder to justify in a rising-rate environment." We find that argument to be short-sighted, and to have little to do with the actual investment merits of innovative businesses that are creating real value in their industries. Therefore, we believe at times like this, when so much of Wall Street and the financial media are reacting in short-sighted ways, it is valuable to share some of our longer-term views on the investment narratives which we see as important drivers of future growth that will play out over the next several years.

One very important development which is sure to bring about many changes is the proliferation of digital currencies utilizing the blockchain, which are poised to disrupt many existing financial structures in payments, and which will enable a proliferation of new business models that will go well beyond finance. Just as the advent of smartphones and of new smartphone apps such as Uber enabled people to use their otherwise-idle cars to earn side income, the advent of blockchains and crypto currencies and tokens can enable people to “rent out” the processing power in their otherwise-idle home computers and game consoles -- and be compensated for their use!

This example is related to the development of the next iteration of internet evolution, sometimes dubbed "Internet 3.0." As this example indicates, Internet 3.0 will likely feature more decentralization, in contrast to the centralization we see today in which giant companies such as Google, Amazon, Twitter and Facebook have disproportionate power and control over monetization and distribution of data and information.

Internet 3.0 will also almost certainly be more "three-dimensional" than the current "two-dimensional" web, which today is still dominated by "flat" web-pages and social media feeds, but which in the future will probably incorporate immersive, three-dimensional virtual spaces ("virtual reality") and "augmented reality" (the addition of visual, digital images and information onto the three-dimensional "real world" with which we are already familiar).

These benefits go far beyond the kind of entertainment and gaming applications that most people think of when they hear "AR" and "VR" mentioned (augmented reality and virtual reality). For example, imagine if an engineer could simply look at the gauge on a high-pressure pipe -- even from a distance -- and immediately get a reading of the pressure and volume and flow of the fluid in that pipeline, presented in a digital visual display floating in his or her field of vision, perhaps while wearing a pair of smart glasses. We believe that industrial and business applications for such technology will be tremendous, and that their potential is only barely appreciated today.

Similarly, we also see an ongoing trend that involves the continued incorporation of the many benefits of digitization and modern technology by industries outside of the traditional "tech sector" which in many cases have yet to take advantage of all the transformative power that technology has to offer. There remain an enormous number of "analog" processes and procedures in industries from education to restaurants to construction which can become digital, with potentially transformative impacts for the companies involved.

We also predict a tremendous increase in the automation of manufacturing, with robotic machinery that will be connected via digital networks. In fact, we think that it is very likely that the much-discussed advent of 5G cellular networks will be most useful for controlling machinery and equipment in major industrial settings, even though most investors think of consumer uses when they hear the word "5G."

And, we see tremendous innovation taking place in the field of medical device technology, including the continued development of minimally-invasive procedures to replace treatments that in the past required much more invasive treatments and much longer recovery times. We are also convinced that the early advances in robot-assisted surgeries and other procedures will only accelerate, as innovative companies find new ways to apply the advantages of new developments in robotic automation to medical applications.

In short, we do not deny that the current investment climate is quite ugly. However, we believe that right now is a very good time to look forward and to realize that the best investment strategy has always involved the identification of what we call "fertile fields for future growth." We are working to include exposure to all of the above growth narratives for our investors -- and to many other themes as well. Thank you for your continued confidence in our firm, and Happy New Year!

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.

Conventional wisdom misses the mark (as usual)

image: Wikimedia commons (link).

The markets are presently selling off sharply, with smaller companies and tech-related companies being sold even more vigorously than the overall market.

The chatter that we are hearing involves three widespread (but, in our opinion, misguided) pieces of "conventional wisdom" on the Street:

- First, that inflation makes smaller companies whose earnings are more "in the future" than "already in hand" significantly less attractive and less valuable,

- Second, that inflation concerns will cause the Fed to raise rates more aggressively which will also negatively impact smaller and more future-oriented companies,

- And Third, that the Omicron variant appears to be much more contagious but much less severe than previous variants, and that if this variant sweeps across the country without causing too much damage, it could create widespread "natural immunity" and thus bring an end to the attractiveness of "Covid-related" stocks, including many technology stocks and the stocks of companies which benefit from the "work from home" and "stay at home" theme.

A look at the performance of various stocks and of various indices over the past several days shows plenty of evidence that the above three pieces of misguided conventional wisdom are behind much of the market action. The Russell 2000 index (a small-cap stock index) has broken blow its 200-day moving average as this post is being published, and other examples could also be offered.

But while there is no denying the spread of either inflation or of a highly-contagious variant in recent weeks, we would argue that the above interpretations miss the mark completely regarding what all this means for smaller, more innovative, and more technology-oriented companies.

First, we of course agree that inflation is an extremely negative development, and one that doesn't help most businesses and certainly doesn't help the general standard of living. However, we completely disagree with the conventional wisdom that argues that in an inflationary environment, it is better to invest in the stocks of "cyclical" and "defensive" companies, and to sell the shares of smaller companies (and especially smaller companies whose growth and earnings is more skewed towards the future).

We understand where this thinking comes from -- but we simply disagree with it.

Based on our experience as professional portfolio managers for going on four decades, in an inflationary environment, we would much rather own the shares of innovative and well-run businesses which are positioned in front of the narratives that are most likely to succeed over the next five to ten years, versus just about any other asset anyone else can suggest (including cash)!

And, as for the convoluted "Omicron" argument which some of the "hot money" on Wall Street are using to guide their so-called "investment decisions" (more accurately, their computer-trading algorithms), we would of course welcome anything that helps bring an end to the lockdown mania that has taken control of the thinking of so many technocrats around the world (and here in the United States).

But while we can't stop algorithmic traders from selling stocks based on their attempts to predict the end of the "Covid story," we think it is a particularly egregious example of the kind of non-fundamental speculation that drives so much of the market action today -- speculation that is extremely unproductive and which real investors should shun.

As we have explained many times in this blog over the years (now going strong since 2007: fifteen years!), our strategy is based on owning well-run businesses in front of future fields for future growth.

It just so happens that the narratives we identified regarding the future were, in almost every case, accelerated by the events of the past two years, but that only goes to show that those narratives we identified were correct descriptions about the way that technology would play a bigger role in more areas of our life in the future (the lockdowns only made that happen faster than it would have otherwise).

We find it to be ridiculous to think that, just because the damaging and (we would argue) nonsensical lockdowns might finally be coming to an end, investors should get rid of any stocks that are involved in the very narratives which are most likely going to continue for many years to come.

As an important aside, we do also recognize that the valuations of some of the companies we own did indeed get carried higher than they should have during the Covid-story-based buying during 2020 and early 2021. Now many of those valuations are being taken down severely. But this kind of over-reaction (in both directions) just underscores the necessity of our standard practice of owning good companies through the various market cycles, for as long as they remain well-managed businesses in front of fertile fields for growth.

And so, during the current market correction, we would advise real investors to avoid getting caught up in mistaken conventional talking points which miss the mark when it comes to the kinds of companies that are best to own for the future. We would be using this "growth correction" to deploy idle cash.

Disclosures: Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Taylor Frigon Capital Management LLC (“Taylor Frigon”), or any non-investment related content, made reference to directly or indirectly in this blog will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this blog serves as the receipt of, or as a substitute for, personalized investment advice from Taylor Frigon. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to his/her individual situation, he/she is encouraged to consult with the professional advisor of his/her choosing. Taylor Frigon is neither a law firm nor a certified public accounting firm and no portion of the blog content should be construed as legal or accounting advice. A copy of the Taylor Frigon’s current written disclosure Brochure discussing our advisory services and fees is available upon request. If you are a Taylor Frigon client, please remember to contact Taylor Frigon, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services.