We've written at least two times previously on the topic of commodities (see here and here). When commodities such as gold and other metals begin to skyrocket, gold advertisements begin to flood the radio stations and financial television shows, and investors inevitably begin to ask themselves, "What about commodities?"

Investors are understandably concerned about the precipitous decline of the dollar. We have been cautioning investors for some time that Fed "oversteering" is probably in the works, based on certain economic beliefs held by Chairman Bernanke which, in our opinion, are misguided (see for greater detail the discussions in "Stand still, little lambs, to be shorn" and "A Phillips-curve Fed?" among many other previous posts). When investors are worried about inflation, or the future of the dollar, gold is one of the first thoughts that enter their minds.

However -- and this may be a little bit counter-intuitive -- this is exactly why they should not rush into commodities without a full understanding of the way they work. The fact that the Fed's oversteering is responsible for gold's recent rise should cause investors to realize that it can tumble just as fast when Fed policy inevitably swings back the other direction.

Back in the middle of last year, with crude prices at $135 a barrel, we made the exact same warning (see here). At the time, as it always does when prices are rising sharply, it felt as though oil prices would never turn around. Of course, they subsequently tumbled below $40 a barrel.

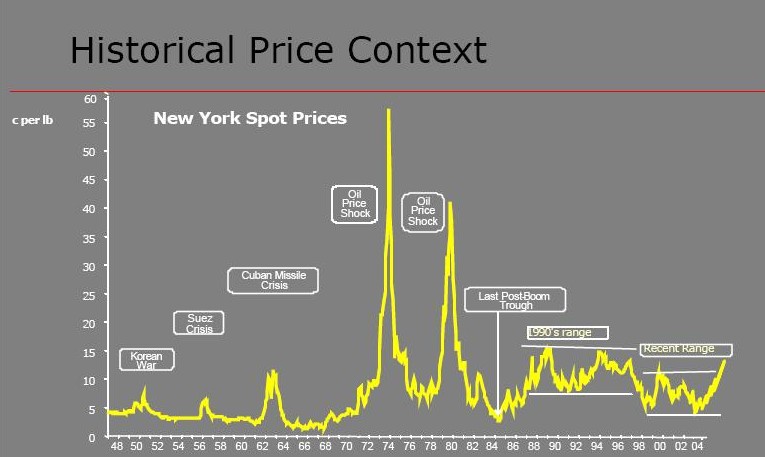

The important point about commodities, which we made in those two previous editions of "What about commodities?" is that they can be quite volatile over time but don't tend to make much progress (see, for example, this chart of sugar prices going back to 1948). Therefore, the only way to make money in them is to attempt to trade the peaks and valleys, hoping to catch them at the right time.

While many believe that the same can be said of owning stocks, in reality owning innovative companies is quite different. Unlike the chart of a commodity that fluctuates back and forth without making real progress, a successful business is creating new value and -- although there will be ups and downs -- the overall trend of such a company tends to be upward over time.

As we've said many times before -- regardless of the economic environment -- owning innovative, growing, well-run businesses is the best foundation for long-term wealth preservation and wealth creation.

Subscribe to receive new posts from the Taylor Frigon Advisor via email -- click here.

For later posts dealing with this same topic, see also:

For later posts dealing with this same topic, see also:

- "Avatar and long-term inflation" 03/02/2010.

- "Gold versus Apple" 10/25/2010.

- "Inflation is a monetary phenomenon" 03/07/2011.

{kind=link}

0 comments:

Post a Comment